Print Story

X

The problem is not insufficient taxpaying capacity; it is the state’s reluctance to tax the privileged sources of income and wealth

| T |

he current tax policy has only one apparent aim: meeting the revenue targets imposed by the International Monetary Fund, even at the cost of undermining productivity. Many of the taxes are oppressive, inflationary, anti-investment and anti-growth. They penalise documented businesses, discourage investment, suppress consumption and reduce competitiveness.

Pakistan is not a poor country. However, it is a poorly governed country. While governments impose ever-higher tax rates in some sectors, significant taxpaying capacity of the economy remains largely untapped.

An alternative tax system based on lower rates, a broader base and predictability can generate revenues in excess of Rs 30 trillion annually while simultaneously promoting economic growth, investment, employment and inclusive development. The Finance Bill 2026 contains no serious move towards that objective. It continues the practice of squeezing the existing taxpayers rather than bringing untaxed wealth, rent and privilege into the tax net.

The federal budget for the year 2026-27 lays bare the nature of Pakistan’s fiscal crisis. Out of the total current expenditure of Rs 17.495 trillion, debt servicing is budgeted at over Rs 8.054 trillion. Creditors will be paid half of what the state collects. Tax policy is thus no longer designed to promote growth or equity; it is increasingly shaped to meet debt obligations and IMF performance benchmarks.

The question is no longer, whether the system is failing. The question is how to replace it. The first step is recognising a simple reality: Pakistan’s fiscal crisis is not a revenue crisis; it is a policy crisis.

The Federal Board of Revenue was originally assigned a collection target of Rs 14.131 trillion for the outgoing fiscal year. After missing even the revised target of Rs 12.983 trillion, it has now been assigned an even higher target of Rs 15.294 trillion for FY 2026-27. Even by imposing some of the highest effective tax burdens in the region, at 11 percent, Pakistan’s tax-to-GDP ratio remains far below the level warranted by its taxpaying capacity. Businesses complain of excessive taxation; governments complain of insufficient revenue. Both are right.

The explanation lies in the structure of taxation. Nearly 95 percent of income tax collection is now realised through withholding and advance tax mechanisms. A substantial part of overall revenues comes through indirect taxes, import-stage taxation and presumptive levies.

These taxes are administratively convenient but economically harmful. They increase production costs, fuel inflation and disproportionately burden low- and middle-income households. The result is an extractive state. Those already documented bear increasing burdens while vast reservoirs of taxpaying capacity remain untouched.

Pakistan’s GDP is Rs 126.9 trillion. Conservative estimates based on national income accounts, sectoral output and consumption data indicate that a modern broad-based tax system can generate over Rs 30 trillion annually without imposing confiscatory rates. The problem is not insufficient taxpaying capacity but the state’s reluctance to tax privileged sources of income and wealth.

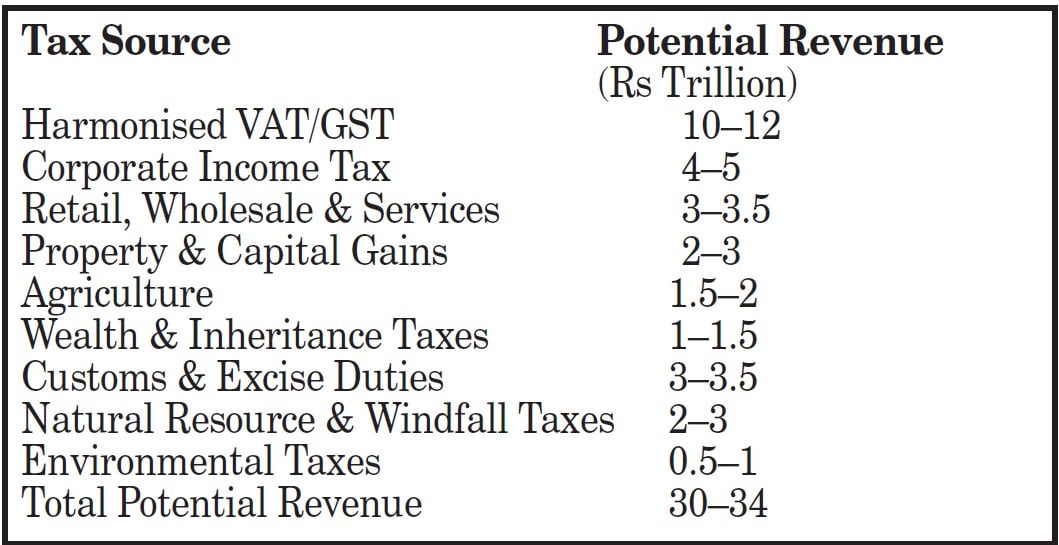

Agricultural income, despite constitutional recognition as a taxable source, contributes only a negligible amount to national revenues. Large absentee landowners, commercial farming enterprises and agricultural rent remain substantially undertaxed. Effective enforcement by provinces can generate well over Rs 1.5 trillion annually.

Likewise, real estate speculation remains one of the largest reservoirs of untaxed or lightly-taxed wealth. Successive governments have preferred transaction taxes and withholding taxes instead of taxing actual gains and economic rent. A rational property taxation framework can yield between Rs 2 trillion and Rs 3 trillion annually while simultaneously discouraging speculative land hoarding and promoting productive investment.

The following estimates illustrate Pakistan’s realistic revenue potential under a low-rate, broad-based and predictable tax regime:

The authors in Towards Broad, Flat, Low-rate and Predictable Taxes and subsequent analyses of FBR’s revenue performance, have presented detailed calculations supporting these estimates. The significance of these estimates lies not merely in the numbers but in the philosophy behind them. Pakistan is currently attempting to extract over Rs 15 trillion from a shrinking documented economy through coercive taxation.

The alternative framework seeks to generate more than double that amount by expanding the economy. The former taxes production; the latter taxes income. The former penalises investment; the latter rewards it. The former protects privilege and untaxed rent; the latter distributes the tax burden according to ability to pay. Most importantly, the former perpetuates dependence on external creditors while the latter creates the fiscal space necessary for economic sovereignty.

Retail and wholesale sectors provide a striking example of policy failure. Despite accounting for a substantial share of economic activity, the sector remains largely outside the formal tax net. Instead of integrating this segment into a modern documentation framework, the government has chosen accommodation.

Under the newly-announced simplified regime, traders with turnover up to Rs 200 million can pay a nominal levy of one percent of gross receipts or Rs 25,000 - whichever is higher - and remain outside meaningful audit, digital integration and monitoring mechanisms. This effectively exempts millions of commercial electricity users from meaningful documentation despite their continuous presence in FBR databases through withholding taxes on electricity, mobile phones, banking transactions and imports.

If large segments of trade remain outside supply-chain digitisation, the entire process of electronic invoicing and digital integration will fail. Universal digital invoicing combined with simplified turnover-based assessments can conservatively generate annual revenues exceeding Rs 3 trillion from this sector alone.

The corporate sector presents a different challenge. Pakistan taxes documented corporations at rates that discourage investment while simultaneously granting exemptions, concessions and preferential treatments to favoured sectors. Lower rates and elimination of distortive tax expenditures can increase compliance, attract investment and broaden the tax base. Corporate income taxation alone can generate Rs 4 trillion to Rs 5 trillion annually.

The greatest opportunity, however, lies in sales taxation. Pakistan’s fragmented sales tax regime has become a nightmare for businesses. Multiple authorities, overlapping jurisdictions, inconsistent procedures and differing interpretations have raised compliance costs and reduced efficiency.

A harmonised value-added tax with a single national administration, broad coverage and moderate rates can generate over Rs 10 trillion annually. Such a system will eliminate cascading taxes, reduce litigation, facilitate inter-provincial commerce and promote documentation throughout the supply chain.

Petroleum taxation provides another example of policy irrationality. The state increasingly relies on petroleum levy because it remains outside the divisible pool. Citizens pay more at fuel pumps and provinces are deprived of their legitimate share under the constitutional framework. This approach may satisfy short-term fiscal targets but undermines both federalism and economic growth. The solution lies in restoring transparent taxation while reducing reliance on hidden levies and para-fiscal charges.

The abolition of undesirable withholding and advance tax provisions that have transformed taxation into a system of presumptive/minimum collections is equally important.

A modern tax administration assesses income rather than taxing transactions. Pakistan’s obsession with withholding taxes has produced a culture of over-taxation for compliant sectors while leaving substantial informal economic activity untouched.

The economic consequences are visible everywhere. Exports remain stagnant. Industrial growth stays weak. Productivity growth is among the lowest in Asia. Investment as a percentage of GDP continues to lag behind rival economies. Young entrepreneurs are increasingly seeking opportunities abroad. The state’s response is invariably the same: impose more taxes on those already paying.

This is precisely the opposite of what successful economies have done. Countries that escaped debt dependence and achieved sustainable growth relied upon low-rate, broad-based and predictable taxation. They encouraged production rather than punishing it. They taxed economic rent instead of productive investment. They rewarded documentation through simplicity rather than coercion.

The writers are lawyers, adjunct faculty at Lahore University of Management Sciences and members of the Advisory Board of Pakistan Institute of Development Economics