Dr Sohail Munir, founding chairperson of the Pakistan Digital Authority, recently argued that Pakistan needs to build an operating system, not another app. He generously cited my earlier piece on UltraApps in making his case. We agree on the architecture. But I want to pose a question that neither of us has fully addressed(yet): Who exactly are we building this for?

The assumption, implicit in most digital policy discussions, is that Pakistan’s digital infrastructure serves Pakistanis. That is necessary but insufficient. If Pakistan is serious about the prime minister’s Rs8.4 trillion ($30 billion) digital export target, we need to stop thinking of ourselves as a market and start thinking of ourselves as a platform, one that can serve the next billion digital users across the Gulf, Africa, Central Asia and the broader Muslim world.

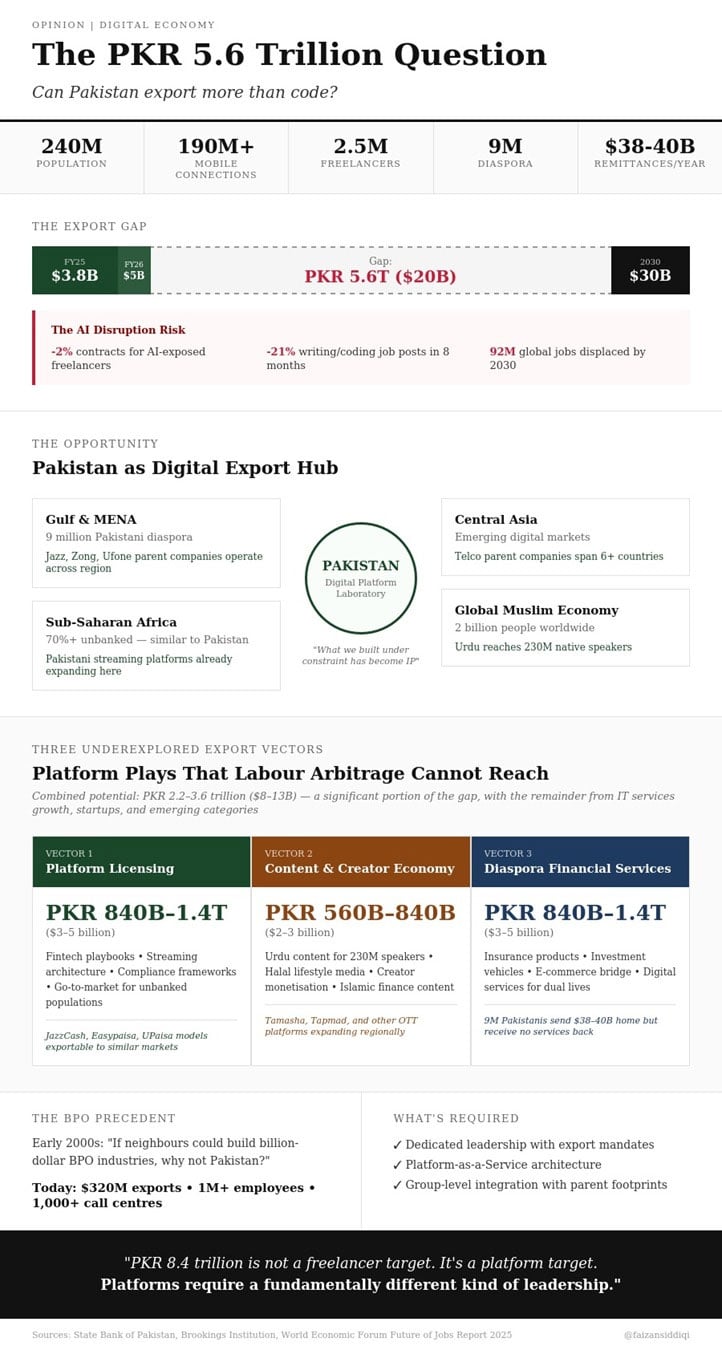

Pakistan’s IT exports reached approximately $3.8 billion in fiscal year 2025, with strong momentum continuing into FY26 towards $4-5 billion. Freelancer inflows have shown exceptional growth, $557 million in just the first half of FY26. The trajectory towards Rs1.4 trillion ($5 billion) this fiscal year looks achievable, built on the talent of 2.5 million freelancers and a growing IT services sector.

But here is the arithmetic problem: Rs8.4 trillion ($30 billion) by 2030 requires more than tripling current exports in four years. The freelancer model, however successful, faces natural constraints: it scales linearly with headcount, competes primarily on labour arbitrage and builds limited durable advantage. We cannot train our way to Rs8.4 trillion. We need a fundamentally different export category.

What if we exported platforms, not just people? Consider what Pakistan has actually built. Our three major telecommunications groups, Jazz, Zong and the emerging PTCL-Telenor entity, collectively serve over 190 million connections. Between them, they operate fintech platforms processing trillions in transactions annually, streaming services reaching tens of millions, enterprise cloud infrastructure, insurance products covering millions of policies, and education. Each sits within a multinational parent: VEON across six countries, China Mobile globally, and e& across the Middle East and Africa.

These are not just Pakistani businesses. They are research and development laboratories for emerging market digital services. The fintech playbooks that work for historically high levels of unbanked populations in Lahore also work in Lusaka. The streaming platforms built for mobile-first audiences in Karachi can serve Karaganda. The micro subscription models enabled by carrier billing are applicable across markets in Africa and Central Asia, where credit card penetration is similarly low.

Pakistan has spent a decade building digital infrastructure under constraints: no PayPal, no Stripe, restricted international payment flows, regulatory complexity. These constraints forced innovation. Local fintech platforms emerged because global ones would not serve us. Carrier billing became sophisticated because card payments were not viable for most. What looked like disadvantage has become intellectual property.

If IT services can plausibly reach Rs2.8 trillion ($10 billion) by 2030, the remaining Rs5.6 trillion ($20 billion) must come from somewhere new. I see three vectors that remain largely undiscussed in policy circles.

First, platform licensing and technical services. Pakistan’s fintech, streaming, and lifestyle platforms represent operational playbooks for serving unbanked, mobile-first populations at scale. These can be licensed to operators across Africa, Central Asia and frontier markets in the Middle East – not as software code, but as turnkey operational models including technology, compliance frameworks, and go-to-market strategies. The addressable opportunity is Rs840 billion to Rs1.4 trillion ($3-5 billion) annually by 2030. Our telecommunications groups already have parent companies operating in these markets. The distribution exists. What is missing is the commercial mandate to treat Pakistani platforms as export products by adding the feature sets they lack.

Second, content and creator economy exports. Pakistan has 71 million YouTube users, making it one of the largest content-creation bases in the world. Yet we have built no infrastructure for Pakistani creators to monetise regional and global audiences. Urdu content reaches over 230 million native speakers, and the global Muslim population represents a vastly underserved market for halal lifestyle content, Islamic finance education, and culturally resonant entertainment. This is a Rs560 billion to Rs840 billion ($2-3 billion) export opportunity.

Third, diaspora financial services. Nine million Pakistanis abroad send home $38-40 billion annually in remittances. The current model treats diaspora as a source of inbound capital. But diaspora populations need financial services too: insurance products aligned with their values, investment vehicles linked to home markets, and e-commerce access to Pakistani goods. Pakistani platforms can serve these nine million customers directly. The opportunity is Rs840 billion to Rs1.4 trillion ($3-5 billion) in diaspora-focused digital financial services.

Together, these three vectors could contribute Rs2.2-3.6 trillion ($8–13 billion) annually by 2030. The remainder will come from continued IT services growth, emerging startups, and categories yet to be defined. The point is not precision but direction. These are the plays that platform thinking unlocks.

Capturing these vectors demands a different organisational model. Today, most digital and lifestyle businesses within Pakistani operators are structured as domestic revenue lines. Entertainment is a tool to reduce churn, not an export product. Fintech is measured on domestic wallets activated, not international expansion potential.

The shift required is from cost-centre thinking to export-platform thinking. This means commercial leadership with explicit international mandates. It means platform-as-a-service architecture, asking not just ‘how do we serve Karachi?’ but ‘how does what we built for Karachi serve Kampala?’ It means integration at the group level, connecting Pakistani platforms to parent companies’ multi-country footprints. We have to move from business-unit economics to venture-building economics.

There is also an uncomfortable truth we must confront. The labour arbitrage model that has powered our freelance economy is facing an existential reckoning. Research from Brookings shows that freelancers in occupations exposed to generative AI have already experienced a 2.0 per cent decline in contracts and a 5.0 per cent drop in earnings since 2022. Job postings for automation-prone writing and coding work have fallen 21 per cent in just eight months. The WEF projects 92 million jobs displaced globally by 2030.

Pakistan cannot assume the freelancer boom will continue uninterrupted. AI does not care about our labour cost advantage. If we do not bridge this gap with platform thinking that is AI-enabled, we will fall significantly short of our export targets.

This is not a government programme. It is a commercial strategy requiring private-sector leadership with the vision to see Pakistani digital platforms as regional products, not just local utilities, starting with telcos, then moving to banks and other large consumer businesses with lower risk appetites.

Dr Munir’s operating system thesis becomes dramatically more compelling under this framing. Digital identity through NADRA, instant payments through Raast, sovereign cloud infrastructure, 5G spectrum now deployed, all of this represents not just domestic capability but exportable architecture.

Pakistan can become for emerging market digital services what Ireland became for European technology operations and what Singapore became for Asian financial services. The difference is that our export is not a physical location advantage or a tax regime; it is operational knowledge of how to build digital businesses for the next billion users who look more like Pakistanis than Americans or Europeans.

We have spent years building our own digital infrastructure. The more interesting question is whether we have the commercial imagination to realise that what we built for Pakistan could serve a billion more.

The foundation is ready. The markets are underserved. It is our play.

The writer is a strategist focused on digital transformation in emerging markets. He tweets/posts @faizansiddiqi and blogs at: blog.chinookstrategy.com