Blockchain technology and the products and services built around it have become an increasingly important part of the modern digital economy....

COVER STORY

Blockchain technology and the products and services built around it have become an increasingly important part of the modern digital economy. Once confined largely to academic research and specialist financial circles, blockchain has evolved into a technology with applications across multiple industries. Its most famous application, cryptocurrency, has generated both excitement and controversy, challenging traditional ideas about money, ownership and financial transactions.

Although concepts related to digital assets and cryptographic security have existed since the 1970s, blockchain technology gained worldwide attention following the 2008 global financial crisis. The crisis exposed weaknesses in major financial institutions and triggered a significant loss of public confidence in conventional banking systems. As stock markets tumbled and trillions of dollars were wiped from the global economy, many people began searching for alternatives that could offer greater transparency, security and independence from central authorities.

Against this backdrop, a pseudonymous individual or group known as Satoshi Nakamoto published a groundbreaking white paper in 2008 titled ‘Bitcoin: A Peer-to-Peer Electronic Cash System’. The paper proposed a decentralised payment system that would allow people to transfer value directly to one another without relying on banks or financial intermediaries. What initially appeared to be an experimental idea would eventually spark a technological revolution that continues to influence finance, business and even government policy today.

At the heart of Bitcoin lies blockchain technology. A blockchain is essentially a digital ledger that records transactions across a network of computers. Unlike traditional databases that are managed by a central authority, a blockchain is distributed among numerous participants. Every participant maintains a copy of the ledger, making the system transparent and significantly more resistant to manipulation.

The term "blockchain" comes from the way information is stored. Transactions are grouped together into blocks, and each block is linked to the previous one using cryptographic techniques, creating a continuous chain. Once a block has been added, altering its contents becomes extremely difficult because doing so would require changing every subsequent block and obtaining agreement from the majority of the network.

Blockchain combines three important elements: cryptography, distributed networks and consensus mechanisms. Cryptography protects information through advanced mathematical techniques. Distributed networks ensure that no single institution controls the entire system. Consensus mechanisms enable participants to agree on the validity of transactions without relying on a central authority.

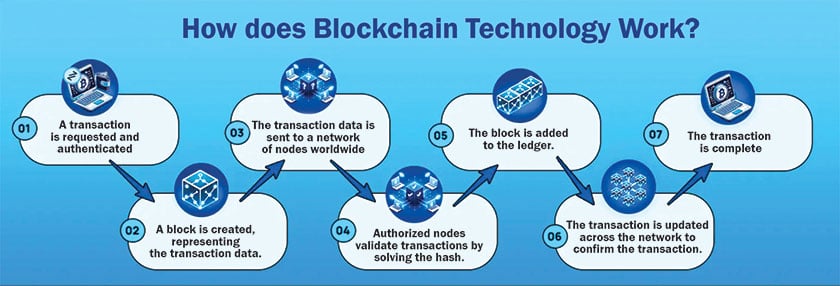

To understand how blockchain works, consider a Bitcoin transaction. When a person sends Bitcoin to another user, the transaction is broadcast to a network of computers known as nodes. The transaction contains information about the sender, the recipient and the amount being transferred. It is also secured using a digital signature generated through cryptographic keys.

Each user possesses a public key and a private key. The public key functions similarly to an account number and can be shared with others. The private key, however, must remain confidential because it is used to authorise transactions. When a transaction is initiated, nodes on the network verify that the sender owns the funds being transferred and that the transaction complies with the network's rules.

Once verified, the transaction is grouped together with others into a block. Before this block can be added to the blockchain, the network must agree that it is valid. This is where consensus mechanisms come into play. Among the various consensus methods developed over the years, the two most widely known are Proof of Work (PoW) and Proof of Stake (PoS).

Proof of Work was the original consensus mechanism introduced by Bitcoin. In this system, specialised computers known as miners compete to solve complex mathematical puzzles. Solving these puzzles requires substantial computing power and energy. The first miner to solve the puzzle earns the right to add the next block to the blockchain and receives a reward in the form of newly created cryptocurrency and transaction fees.

The puzzle-solving process involves generating a value known as a nonce and repeatedly modifying it until the resulting cryptographic hash meets specific network requirements. Although this process may sound complicated, its purpose is straightforward: to make fraudulent activity prohibitively expensive and difficult. The enormous amount of computing power required to alter transaction records serves as a powerful security mechanism.

Despite its effectiveness, Proof of Work has attracted criticism because of its high energy consumption. As environmental concerns have grown, many blockchain projects have sought alternatives that offer similar security while requiring significantly less electricity.

One such alternative is Proof of Stake. Under this mechanism, participants known as validators lock up, or stake, a portion of their cryptocurrency as collateral. Instead of competing through computational power, validators are selected to verify transactions based on factors determined by the network's algorithm. Honest validators receive rewards, while dishonest participants risk losing part of their stake.

Ethereum, the world's second-largest blockchain network, successfully transitioned from Proof of Work to Proof of Stake. Supporters argue that this approach dramatically reduces energy consumption while maintaining network security.

Although blockchain technology has numerous applications, cryptocurrencies remain its most widely recognised use case. Cryptocurrencies are digital assets that operate on blockchain networks and can be transferred directly between users. Thousands of cryptocurrencies now exist, each designed with different goals and features.

Among the most important categories are stablecoins. Unlike traditional cryptocurrencies that often experience dramatic price fluctuations, stablecoins are designed to maintain a relatively stable value. They achieve this by linking their value to an existing asset, most commonly a national currency such as the US dollar.

One well-known example is USDT, issued by Tether. The objective of stablecoins is to combine the speed and efficiency of blockchain technology with the price stability associated with traditional currencies. This makes them particularly useful for payments, remittances and trading activities.

Bitcoin differs significantly from stablecoins because it is not directly backed by a government-issued currency or physical asset. Instead, its value is determined by supply, demand and market sentiment. This characteristic contributes to Bitcoin's appeal as a speculative investment but also explains its considerable volatility.

Beyond digital currencies, blockchain is increasingly being used to transform traditional financial markets through a process known as tokenisation. Tokenisation involves representing real-world assets digitally on a blockchain. These assets can include stocks, bonds, artwork, commodities and real estate.

The concept has attracted considerable attention because it can make investing more accessible. Instead of purchasing an entire property or expensive asset, investors can buy small fractional ownership stakes represented by digital tokens. This lowers barriers to entry and enables broader participation in investment opportunities that were previously available only to wealthy individuals or institutions.

The Gulf region has emerged as one of the leaders in this field. Recently, a property in Dubai was tokenised and offered to investors through a digital platform. The project attracted significant attention because it demonstrated how blockchain technology could enable fractional ownership and expand access to real estate investment.

Another important feature of blockchain technology is the smart contract. A smart contract is a self-executing digital agreement that automatically performs specific actions once predetermined conditions have been met. Because these agreements operate according to code rather than manual intervention, they can reduce administrative costs, minimise delays and lower the risk of fraud.

Smart contracts have applications far beyond cryptocurrency. They can be used in insurance, supply chain management, healthcare, property transactions and numerous other sectors. As blockchain technology continues to mature, smart contracts are expected to play an increasingly significant role in automating business processes.

Governments and regulators around the world have gradually shifted from scepticism towards cautious engagement with blockchain technology and digital assets. Countries such as Singapore, the United Kingdom, the United States and the United Arab Emirates have introduced regulatory frameworks aimed at encouraging innovation while protecting consumers and maintaining financial stability.

Pakistan has also signalled its intention to regulate the cryptocurrency sector and align it with international anti-money laundering and know-your-customer standards. The establishment of the Pakistan Virtual Asset Regulatory Authority represents an important step towards bringing greater oversight and legitimacy to the country's growing digital asset ecosystem.

However, challenges remain. Cryptocurrency markets continue to experience significant volatility. Cybersecurity threats, scams and fraudulent investment schemes remain persistent concerns. Regulatory uncertainty in some jurisdictions also creates obstacles for businesses and investors seeking to participate in the industry.

Despite these challenges, blockchain technology continues to evolve at a remarkable pace. Supporters believe it has the potential to reshape industries by increasing transparency, improving efficiency and reducing reliance on intermediaries. Critics remain cautious, pointing to unresolved issues related to regulation, scalability and security.

Regardless of where one stands in this debate, blockchain has already demonstrated its ability to influence the way people think about money, ownership and digital interaction. What began as the foundation of Bitcoin has expanded into a technological movement with applications reaching far beyond cryptocurrency.

As innovation continues and adoption grows, blockchain may become as commonplace as the internet itself. Whether it ultimately fulfils all of its ambitious promises remains to be seen, but one thing is certain: blockchain technology is no longer a fringe concept. It has become a significant force in the modern digital economy and is likely to play an important role in shaping the future.